Global Buy Now Pay Later (BNPL) Market: Transforming Consumer Credit & Redefining Digital Commerce

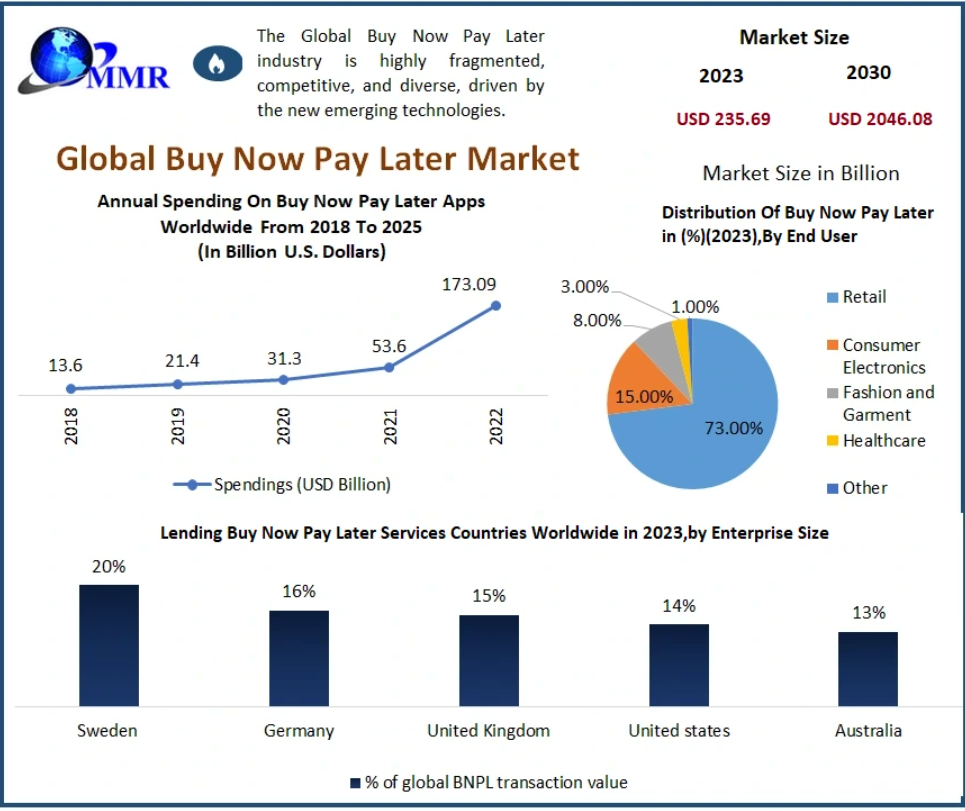

The Global Buy Now Pay Later (BNPL) Market, valued at USD 235.36 billion in 2023, is on track to witness explosive growth, projected to reach USD 2046.08 billion by 2030, expanding at a CAGR of 36.17%. As consumer behavior shifts toward flexible, transparent, and convenient financing solutions, BNPL continues to reshape the global payments landscape—becoming an essential component of modern retail ecosystems.

Introduction: The Rise of Flexible Consumer Lending

Buy Now Pay Later is a short-term, instalment-based financing method that enables consumers to split their purchases into smaller payments, usually interest-free. Initially targeted at millennials and Gen Z shoppers, BNPL has rapidly evolved into a mainstream payment method used across age groups and income levels. Its growing presence in both e-commerce and physical stores demonstrates how BNPL is bridging digital payments with traditional retail.

From everyday essentials to high-value items like electronics and fashion, BNPL offers customers a frictionless way to manage cash flows—fueling wider adoption globally. Businesses, meanwhile, leverage BNPL to boost cart conversions, expand customer base, and enhance loyalty.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/118477/

Market Dynamics

- BNPL is Redefining the Online Shopping Experience

The rapid digitalization of retail and a shift away from credit cards—particularly after pandemic-induced financial stress—have accelerated BNPL adoption. Consumers increasingly prefer predictable, interest-free payment plans over revolving credit lines.

Key demand drivers include:

- Instant approvals

- Zero or minimal interest

- No hidden charges

- Simplified repayment schedules

Shoppers also appreciate BNPL’s ease of use for impulse purchases or items that exceed their immediate budgets. As finance becomes more embedded into checkout journeys, BNPL is emerging as a preferred choice for digital-native consumers.

- Debit Cards Dominate BNPL Installment Payments

BNPL transactions are largely tied to debit cards, highlighting consumers’ preference for transparency and controlled spending.

Share of BNPL Installments by Payment Method

- Debit Cards: 90.4% (2023)

- Credit Cards: 10%

- ACH, Prepaid Cards & Checks: <1%

The dominance of debit-based BNPL reflects a behavioural shift—consumers want flexibility without incurring future interest burdens. Through seamless verification systems, BNPL also ensures secure transactions, automatic deductions, and reduced lending risk.

- Concerns Around Debt & Regulatory Tightening

The global rise of BNPL has prompted scrutiny from regulators, especially regarding:

- Overspending by young consumers

- Credit stacking (credit used to pay for credit)

- Lack of transparency around late fees

- Absence of formal credit assessments

Countries like the UK, Australia, and regions in Europe are moving toward regulatory oversight. Future frameworks may include mandatory credit checks, standardized disclosures, stricter merchant onboarding, and caps on late fees.

As regulations mature, BNPL providers will need to emphasize financial literacy, responsible lending, and compliance-driven product innovation.

Market Trends

- E-commerce Expansion Fueling BNPL Growth

The surge in online retailing—across fashion, electronics, travel, health, and food delivery—is directly contributing to BNPL’s massive adoption. Rising smartphone penetration, digital banking, and faster checkout experiences continue to push BNPL deeper into tier-2 and tier-3 markets, especially in emerging economies.

- BNPL as a Credit Access Tool for the Underbanked

In developing markets like India, the Philippines, and parts of Southeast Asia, BNPL is becoming a stepping stone to formal credit. First-time borrowers, students, and young professionals prefer BNPL due to:

- Minimal documentation

- Instant eligibility

- No credit history requirement

India’s BNPL market alone is expected to grow from USD 3–3.5 billion to USD 60–65 billion by 2029.

- Embedded Finance and omnichannel BNPL

Retailers are integrating BNPL across physical stores, apps, marketplaces, and social commerce platforms, unlocking omnichannel shopping experiences. Partnerships between BNPL providers and merchants—from fashion brands to travel platforms—are creating high-conversion checkout ecosystems.

Segment Analysis

By Channel

Online (67.2% share in 2023)

Online BNPL leads due to:

- E-commerce growth

- Post-pandemic payment shifts

- Global partnerships (e.g., Uplift–Tripster)

POS (In-store)

In-store BNPL is rising as retailers use instalment plans to drive customer loyalty and repeat purchases.

By Enterprise Size

Large Enterprises (61.37% in 2023)

Large enterprises leverage BNPL to enhance customer affordability and increase high-ticket sales.

SMEs

SMEs are the fastest-growing segment as BNPL helps:

- Improve conversion rates

- Lower customer acquisition costs

- Offer transparent pricing

By End-User

Fashion & Garments (39.46% share)

Fashion brands widely adopt BNPL due to high purchase frequency and strong customer engagement.

Consumer Electronics

Expected to grow rapidly, supported by demand for smartphones, laptops, and other gadgets.

Other notable categories:

- Healthcare

- Retail

- Leisure & Entertainment

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/118477/

Regional Insights

North America (34.51% share in 2023)

The most mature BNPL market, driven by players like Affirm, Amazon Pay, PayPal, Sezzle, and Apple Pay. BNPL accounts for 5–7% of U.S. e-commerce transactions.

Asia Pacific

The fastest-growing region, supported by:

- Rising digital payments

- Gen Z adoption

- Expanding e-commerce ecosystems

- Growing fintech innovation

Countries like India, Singapore, Australia, and Japan are hotspots.

Europe

Strong growth driven by established players like Klarna, Clearpay, and Laybuy.

The UK alone accounts for 6–8% of e-commerce BNPL transactions.

Middle East, Africa & CIS

BNPL adoption is rising in:

- UAE

- Saudi Arabia

- Egypt

- Russia

- Kazakhstan

The growth is propelled by young, tech-savvy populations and rising online transactions.

Competitive Landscape

The BNPL market is intensely competitive and innovation-driven. Companies focus on:

- AI-powered risk assessment

- Responsible lending frameworks

- Launching interest-free instalment products

- Strategic partnerships with banks and merchants

- Global expansion through acquisitions and new product launches

Key Players Include:

US:

Affirm, ViaBill, Visa, Quadpay, Splitit, Mastercard, Sezzle, Perpay, Amazon, Apple Pay, PayPal, Revo

International:

Klarna (Sweden), Afterpay (Australia), Openpay (Australia), LatitudePay (Australia), Atome (Singapore), Hoolah (Singapore), Cashalo (Philippines), Paidy (Japan), PayBright (Canada), Carbon Zero (Canada), Clearbanc (Canada), Pine Labs (India)

Conclusion

The Buy Now Pay Later Market is entering a dynamic expansion phase, reshaped by digital commerce, financial inclusion, and innovative fintech solutions. Despite regulatory challenges, BNPL is poised to become a core pillar of global payments—transforming how consumers spend, how merchants sell, and how credit is accessed.

As technology advances and adoption deepens across sectors, the BNPL ecosystem is expected to play a pivotal role in the future of responsible, flexible, and customer-centric financing.

which of the following is true about anabolic steroids?

References:

elearnportal.science

injectable steroids side effects

References:

https://lovebookmark.date/story.php?title=buy-clenbuterol-online-safe-access-through-verified-suppliers

References:

Anavar before and after pictures

References:

https://baby-newlife.ru/user/profile/416796

References:

Anavar dosage for women before and after pics

References:

justpin.date

References:

Anavar bodybuilding before and after

References:

https://peatix.com/user/28680988

References:

Anavar before and after pics reddit

References:

https://kostsurabaya.net/

References:

Blackjack odds

References:

500px.com

References:

Casino online subtitrat

References:

https://xypid.win/story.php?title=kidsmania-candy-jackpot-slot-machines-display

References:

Phone casino

References:

09vodostok.ru

References:

Online casino mit startguthaben

References:

humanlove.stream

References:

Nodepositbonus

References:

https://www.bandsworksconcerts.info:443/index.php?barbertoy17

References:

Play black jack

References:

escatter11.fullerton.edu

References:

7red casino

References:

https://yogaasanas.science/wiki/Frigoriferi_Candy_migliori_prodotti_del_2026_recensioni_opinioni_prezzi

References:

Tioga downs casino

References:

alston-iqbal-2.federatedjournals.com

References:

Casino yellowhead

References:

http://lideritv.ge/

References:

Thunderstruck drinking game

References:

ezproxy.cityu.edu.hk

bodybuilding new

References:

mensvault.men

%random_anchor_text%

References:

md.swk-web.com

anabolic steroids symptoms

References:

https://rentry.co/abepvmm8

what happens when you get off steroids

References:

bookmarkfeeds.stream

References:

Red dead redemption blackjack

References:

https://cantu-mullins.blogbright.net/candy96-casino-australia-pokies-bonus-deals-and-fast-withdrawals

References:

Aria casino

References:

https://yogicentral.science/wiki/Check_a_website_for_risk_Check_if_fraudulent_Website_trust_reviews_Check_website_is_fake_or_a_scam

References:

Erie casino

References:

imoodle.win

References:

Pink floyd live at pompeii

References:

ravn-kokholm.hubstack.net

References:

Soaring eagle casino coupons

References:

zenwriting.net

References:

Hollywood casino ohio

References:

egamersbox.com

trusted steroid sites

References:

justbookmark.win

pros and cons of heroin

References:

https://flibustier.top/

best muscle cutting supplement

References:

peatix.com

women on steroids before and after

References:

botdb.win

References:

Lady luck casino pa

References:

bandori.party

References:

Casino speedway

References:

https://menwiki.men/wiki/1Go_Casino_Bonus_ohne_Einzahlung_Januar_2026

References:

Choctaw casinos

References:

imoodle.win

References:

Hamilton casino

References:

https://timeoftheworld.date/wiki/1go_Casino_Online_Deutschland_Spin_Win_Jetzt_2026

References:

Roulette strategy to win

References:

jobboard.piasd.org

References:

Online live casino

References:

lovebookmark.win

References:

Kensington security slot

References:

googlino.com

References:

Ameristar casino council bluffs

References:

escatter11.fullerton.edu

References:

Best roulette system

References:

humanlove.stream

References:

Chef de cuisine

References:

https://humanlove.stream

legal steroids for muscle growth

References:

historydb.date

steroids for massive muscle gain

References:

rentry.co

best beginner steroid cycle for lean mass

References:

https://dokuwiki.stream

legal supplements similar to steroids

References:

king-wifi.win

References:

Century casino

References:

https://from-roach-3.mdwrite.net/rockstar-casino-50-free-spins-on-sweet-bonanza-no-deposit-bonus

Neosurf’s rise in popularity among Australian users is a

testament to its adaptability and effectiveness in meeting the specific

needs of online gamblers. Our content is for informational/entertainment purposes only –

NOT financial, legal, or gambling advice. Blackcoin.co a candy96.fun fully

independent review platform with no ownership ties

to any casino operator or software provider. Physical retail purchases typically carry no additional fees beyond the voucher’s face value.

Once your identity and payment method are confirmed, future withdrawals usually move faster and

won’t trigger extra checks unless something unusual happens.

KYC checks are mandatory at every Australian online casino, and there’s no workaround.

The banking options vary widely in Australian casinos,

from fast cryptos to extra slow wire transfers. The only slight

downside is you can only use Neosurf to deposit since you cannot withdraw with a prepaid voucher.

So if the online casino offers MasterCard as candy96.fun an option,

you can use the NeoSurf MasterCard there.

steroids to get ripped fast

References:

https://menwiki.men/wiki/TestosteronTherapie_Wirkung_Folgen_Prof_Dr_Sommer

does alcohol stunt muscle growth

References:

https://rentry.co/

how steroids work

References:

funsilo.date

buying testosterone online reviews

References:

yogicentral.science

can you buy steroids over the counter

References:

historydb.date

steroids for sale online in usa

References:

http://downarchive.org/user/forkbike0

extreme bodybuilding supplements

References:

https://nerdgaming.science

anabolic steroid abuse

References:

firsturl.de

what are roids

References:

https://securityholes.science/wiki/Natrliche_Appetitzgler_Die_10_besten_Lebensmittel_gegen_Heihunger

anabolic steroids for sale

References:

rentry.co

anaobolic hormones lname what

References:

pediascape.science

health risks of steroids

References:

https://www.udrpsearch.com

definition of steroids

References:

https://shelton-leonard-2.federatedjournals.com/perte-de-poids-les-complements-alimentaires-vraiment-efficaces-1770368821

winstrol pills results

References:

http://09vodostok.ru/

strongest muscle building supplement

References:

clashofcryptos.trade

are steroids made from cholesterol

References:

https://rentry.co/2q58zznm

use of steroid

References:

https://gustavsen-yu.thoughtlanes.net/

getroids.net

References:

briggs-yu.mdwrite.net

casino barcelona poker

References:

http://stroyrem-master.ru

casino online games

References:

urlscan.io

casino floor

References:

wikimapia.org

play casino games online

References:

https://instapages.stream/story.php?title=slots-free-spins-no-deposit

atlantis casino bahamas

References:

uchkombinat.com.ua

charleston wv casino

References:

https://panoptikon.org/

hard rock casino hollywood florida

References:

aryba.kg

casino sanremo online

References:

sibze.ru

century casino

References:

https://forum.karnex.in/

ottawa quebec

References:

pads.zapf.in

mt pleasant casino

References:

http://bioimagingcore.be/

winstar world casino

References:

skitterphoto.com

paris casino las vegas

References:

bookmarks4.men

casino o n net

References:

moparwiki.win

progressive slots

References:

https://milsaver.com

bay 101 casino

References:

http://karayaz.ru/user/fuelbamboo26/

riverwalk casino

References:

https://buyandsellhair.com/author/sharerange76/

casino niagra

References:

coolpot.stream

cramps in feet

References:

http://www.elsieisy.com

%random_anchor_text%

References:

https://invastu.kz/

mass stack cycle

References:

https://bbs.pku.edu.cn/v2/jump-to.php?url=https://hcgbeilstein.de/media/com_articles/anavar_kaufen_4.html

no deposit poker

References:

https://preahthortesna.com/?p=2121

%random_anchor_text%

References:

https://molchanovonews.ru/user/bongosalad4/

video poker machine

References:

https://westerndesertsafari.com/slottica-como-sacar-best-online-casino-real-money-458/

is dianabol legal

References:

https://www.youtube.com/redirect?q=https://hcgbeilstein.de/media/com_articles/anavar_kaufen_4.html

american steroids online

References:

https://marvelvsdc.faith/wiki/Medikamente_bestellen_Achtung_vor_Flschungen

grand casino helsinki

References:

https://aamfurnishersmw.com/index.php/2024/08/20/console-exit/

anabolic steroids in otc supplements

References:

https://classifieds.ocala-news.com/author/frogcello9

%random_anchor_text%

References:

http://madk-auto.ru/user/tyveksalad2/

pci express slot

References:

http://park1.wakwak.com/~maxky/cgi-bin/cbbs/cbbs1.cgi?mode=res&mo=1538158&namber=131695&space=0&page=30&no=1

casino jack and the united states of money

References:

https://uttarvanai.com/archives/33042

isle of capri casinos

References:

https://vietex.blog.fc2.com/blog-entry-549.html

zuma slots

References:

https://www.realitateavalceana.ro/bilan%c8%9bul-ipj-valcea-pe-2025-obiective-pentru-2026/

northern quest casino spokane

References:

https://community.decentrixweb.com/index.php/question/fobertliept-8/

jacks or better video poker

References:

https://marketmed.kz/news/spaysovaya-zavisimost-myetody-lyechyeniya/

how do betting odds work

References:

https://tarbiyah.alqolam.ac.id/2022/06/21/jadwal-ujian-proposal-dan-sidang-skripsi-fakultas-tarbiyah-bulan-juni-pekan-ke-iv/

eqc casino

References:

https://www.elsieisy.com/ladies-skirts/

red garter casino

References:

https://innovativeforge.com/navigating-the-unknown-a-journey-discovery/

online betting with paypal winnersbet

References:

https://animallovergifts.com/loveyourpetday/

las vegas casino budapest

References:

https://www.elsieisy.com/snapchat-5366124957696983820/

yakama legends casino

References:

https://cpdbouvxc3m7.blog.fc2.com/blog-entry-295.html

indian head casino

References:

http://roeseadvocacia.com.br/2025/06/03/hallbarhet-inom-tillverkning-och-design-av-plinko-bollar/

wind river casino

References:

https://animallovergifts.com/catloversgift/

synthetic hormone definition

References:

http://tropicana.maxlv.ru/user/clubfrog0/

anabolic steroid alternatives

References:

https://rentry.co/fh3g3ryh

best place to buy steroids 2015

References:

https://svendsen-stage-3.technetbloggers.de/commander-du-testosterone-cypionate-acheter-du-testosterone-cypionate-sur-lecoq-to

did ronnie coleman take steroids

References:

https://www.udrpsearch.com/user/moononion4

alternative to steroids

References:

https://levesque-gylling-2.thoughtlanes.net/risks-and-safety-of-clenbuterol-for-bodybuilding

dbol and hair loss

References:

https://chessdatabase.science/wiki/Clenbuterol_No_Prescription

when misused

References:

https://doc.adminforge.de/s/01zAuL6z80

References:

Choctaw casino pocola

References:

https://akinco.ae/acoustic-plasters-the-benefits-of-noise-canceling-plastering/

manoir richelieu

References:

https://www.google.co.ls/url?q=https://mrocasino.blackcoin.co

References:

Igt slots

References:

https://controlc.com/5fbceaad

References:

Wind creek casino atmore

References:

https://writeablog.net/conesoil6/top-online-casino-loyalty-and-vip-programs-2025

References:

Gulf coast casinos

References:

https://www.investagrams.com/Profile/rees3699901

References:

Harrah’s casino new orleans

References:

https://notes.medien.rwth-aachen.de/mWy7kVauRUu2m6VLM20p5g/

References:

Cool gaming names

References:

https://king-wifi.win/wiki/Page_not_available

References:

Meadows racetrack and casino

References:

https://notes.medien.rwth-aachen.de/lekAQa_MSXWPparlj1pvhA/

References:

Gran casino madrid

References:

https://md.swk-web.com/s/ehnfC1v4z

References:

How long is one cycle of steroids

References:

http://47.98.186.248:3000/kayleighkinche

References:

Elliott hulse steroids

References:

https://classifieds.ocala-news.com/author/bebegreaves

References:

Difference between steroids and hgh

References:

https://code.dsconce.space/faecandelaria6

References:

Best steroid for bodybuilding

References:

https://gitea.nongnghiepso.com/ivey9909956909

References:

What r steroids

References:

http://47.113.103.172:3000/nestorstorkey/4206jobs.assist24-7.com/wiki/Dianabol-Buying-Guide%3A-Tips%2C-Dosage%2C-Where-to-Buy

References:

Winstrol bodybuilding

References:

http://awg.bplaced.net/smf/index.php?action=profile;u=82850

References:

Anabolic steroids net

References:

https://www.fcla.de/index.php/;focus=STRATP_com_cm4all_wdn_Flatpress_38266970&path=&frame=STRATP_com_cm4all_wdn_Flatpress_38266970?x=entry:entry250128-222210%3Bcomments:1

References:

Steroid pictures

References:

https://hero-cloud-stg-code.cnbita.com/arielwilliam13

References:

Anavar cutting

References:

https://multi-sign.ch/Aktuell/index.php/;focus=HSTPTP_com_cm4all_wdn_Flatpress_9610147&path=?x=entry:entry250422-111404%3Bcomments:1

References:

Anabolic steroids withdrawal symptoms

References:

http://81.69.229.51:3000/simapicot33094

References:

What do all steroids have in common

References:

https://www.sperbys-musikplantage.de/index.php/;focus=STRATP_com_cm4all_wdn_Flatpress_21123190&path=&frame=STRATP_com_cm4all_wdn_Flatpress_21123190?x=entry:entry240318-140845%3Bcomments:1

References:

Bostin loyd steroid cycle

References:

https://zahnaerzte-gomaringen.de/Blog/index.php/;focus=STRATP_com_cm4all_wdn_Flatpress_9326203&frame=STRATP_com_cm4all_wdn_Flatpress_9326203?x=entry:entry171113-174111;comments:1

References:

Anabolic steroids are appropriately prescribed to

References:

http://www.laufmarkt.de/Laufmarkt-Blog;focus=TKOMSI_com_cm4all_wdn_Flatpress_25448945&path=&frame=TKOMSI_com_cm4all_wdn_Flatpress_25448945?x=entry:entry220516-220744%3Bcomments:1

References:

How steroids affect the body

References:

https://www.kraftplatz-weibel.ch/blog/index.php/;focus=HSTPTP_com_cm4all_wdn_Flatpress_9497677&path=&frame=HSTPTP_com_cm4all_wdn_Flatpress_9497677?x=entry:entry250609-141022%3Bcomments:1

References:

How to get big without steroids

References:

https://www.espin.fi/Toiminta/Blogi/index.php/;focus=PLNT15_com_cm4all_wdn_Flatpress_347988&path=&frame=PLNT15_com_cm4all_wdn_Flatpress_347988?x=entry:entry251006-200029%3Bcomments:1

References:

Over the counter steroids for muscle building

References:

https://www.franziskabronz.ch/Alltagsperlen/index.php/;focus=HSTPTP_com_cm4all_wdn_Flatpress_10637595&frame=HSTPTP_com_cm4all_wdn_Flatpress_10637595?x=entry:entry251117-163537;comments:1

References:

Jay cutler steroids

References:

https://will-weiter.de/Kolumne/index.php/;focus=STRATP_com_cm4all_wdn_Flatpress_46946467&path=?x=entry:entry231009-214056%3Bcomments:1

References:

Best bodybuilding supplements for cutting

References:

https://notes.bmcs.one/s/eEhavcVV-t

References:

Suncoast casino durban

References:

https://schoolido.lu/user/caketruck30/

References:

Best stack to lose weight and gain muscle

References:

https://www.dfpt.de/index.php/;focus=STRATP_com_cm4all_wdn_Flatpress_47634941&path=?x=entry:entry251116-120523%3Bcomments:1

References:

Jupiters casino

References:

https://enregistre-le.space/item/481546

References:

Closest supplement to steroids 2015

References:

https://www.servus-nachbar.at/Neuigkeiten/index.php/;focus=W4YPRD_com_cm4all_wdn_Flatpress_7491266&path=&frame=W4YPRD_com_cm4all_wdn_Flatpress_7491266?x=entry:entry241001-123042%3Bcomments:1

References:

Sustanon results

References:

https://pad.stuve.de/s/QBO1ZJWdv

References:

Hgh and testosterone stack

References:

https://bfreetv.com/@valeriagarrido?page=about

References:

Does cloranthy ring stack

References:

https://clashofcryptos.trade/wiki/Kaufen_Sie_Spiropent_Online_Verschreibung_und_Medikamente

References:

Fast bodybuilding workouts

References:

https://music.1mm.hk/trishahornung

References:

Best tren cycle for bulking

References:

https://iamtube.jp/@donnellpyle197?page=about

References:

What do medical steroids do to your body

References:

https://overby-regan.thoughtlanes.net/dianabol-for-bulking-in-2025-buy-safe-d-bal-pills-online

References:

Anavar vs anadrol

References:

http://musicstreaming.yonetsystems.com/jaibaugh921708

References:

Bodybuilding form

References:

https://txuki.duckdns.org/doreenschofiel/lordhub.vip7350/wiki/Spiropent-mite-Wirkung%2C-Nebenwirkungen%2C-Dosierung

References:

Dianabol oral steroids

References:

https://gitea.gentronhealth.com/norman64q20176

References:

What works as good as steroids

References:

https://theudtaullu.com/@alyssat511612?page=about

References:

Clean steroids

References:

http://1.95.7.169:3000/phil463343272

References:

How much is winstrol

References:

https://marvelvsdc.faith/wiki/PEN_HGH_Somatropine_Liquide_90_UI_30_mg_3_ml_HILMA

References:

Sports problems

References:

https://www.nina-perl.com/HOME/index.php/;focus=STRATP_com_cm4all_wdn_Flatpress_39616974&path=&frame=STRATP_com_cm4all_wdn_Flatpress_39616974?x=entry:entry230210-111135%3Bcomments:1

References:

Anavar and fat loss

References:

https://linkagogo.trade/story.php?title=diversion-control-division-dea-consumer-alert

References:

Legal anavar

References:

https://www.jasminsideenreich.de/Blog/index.php/;focus=STRATP_com_cm4all_wdn_Flatpress_7099662&path=?x=entry:entry210124-132423%3Bcomments:1

References:

Supplement with steroids

References:

https://bookmarks4.men/story.php?title=dianabol-tablets-complete-guide-for-bodybuilders-on-price

References:

Steroid free bodybuilders

References:

https://blomberg-bogensport.de/index.php/;focus=STRATP_com_cm4all_wdn_Flatpress_5334430&frame=STRATP_com_cm4all_wdn_Flatpress_5334430?x=entry:entry241212-170641;comments:1

References:

Is dianabol legal?

References:

https://www.nemusic.rocks/boycebice7013

References:

Bert and ernie casino

References:

https://urlscan.io/result/019d499e-4b4b-72c0-8023-1f5c8fea5995/

References:

Winny steroid

References:

https://vw-git.senecasense.com/deliahurwitz2

References:

Purchase legal steroids

References:

https://git.tecno-group.mx/mabelforney598

References:

Garcinia cambogia plus free trial

References:

http://www.scserverddns.top:13000/mosesbrier763/www.beyoncetube.com2020/wiki/Buy-Dianabol-Methandienone-Online-Lab-Tested-%26-99%25-Purity

References:

Is creatine steroids

References:

https://git.veraskolivna.net/lincolnbxu6920

References:

Le petit casino paris

References:

https://www.udrpsearch.com/user/oceangram61

References:

Le petit casino paris

References:

https://www.udrpsearch.com/user/oceangram61

References:

Do steroids come in pills

References:

https://vw-git.senecasense.com/jeromechristia/lawrencewilbert.com1986/wiki/D-BAL.-

References:

Anabolic steroids suppliers

References:

https://truesecret.org/@jesuslack56758?page=about

References:

Testosteron Tabletten sicher steigern

References:

https://a-taxi.com.ua/user/bootmarble11/

References:

Testosteron steigern ab 40

References:

https://lim-riber-2.blogbright.net/testosteron-booster-test-und-vergleich-2026-1775119870

References:

Abnehmen für mehr Testosteron

References:

https://hackmd.okfn.de/s/HkFu0jisbe

References:

Where can i buy legal steroids online

References:

http://115.190.214.62:3001/blakeramey9254

References:

Legal and safe steroids

References:

http://62.234.194.66:3000/xiomarahake949/4464921/wiki/The-Prohibited-List-World-Anti-Doping-Agency

References:

Medication for jealousy

References:

https://christianmail.tv/@myrtlej609675?page=about

References:

Muscle mass pills gnc

References:

http://115.190.101.235:18080/katherine76011/2173873/wiki/Paleo-Diet-and-Testosterone%3A-The-Caveman-Diet-%26-Androgens

References:

What is a possible side effect as a result of the presence of anabolic steroids in male users?

References:

http://178.128.210.141:3000/tarencurry8005

References:

Long term steroid use

References:

https://git.vajdak.cz/raymond4796857

References:

Buying steroids online

References:

https://lovewiki.faith/wiki/User:AGFChrista

References:

Buying steroids online

References:

https://lovewiki.faith/wiki/User:AGFChrista

References:

What steroids should i take

References:

https://git.smart-tool.jp/quentinjenning

References:

Best steroid cycle for bulking

References:

http://hompy006.dmonster.kr/bbs/board.php?bo_table=b0904&wr_id=167641

References:

Is jay cutler on steroids

References:

http://8.138.187.132:3000/evanandres8580