Automotive Market in India – A Fresh and Unique Analysis

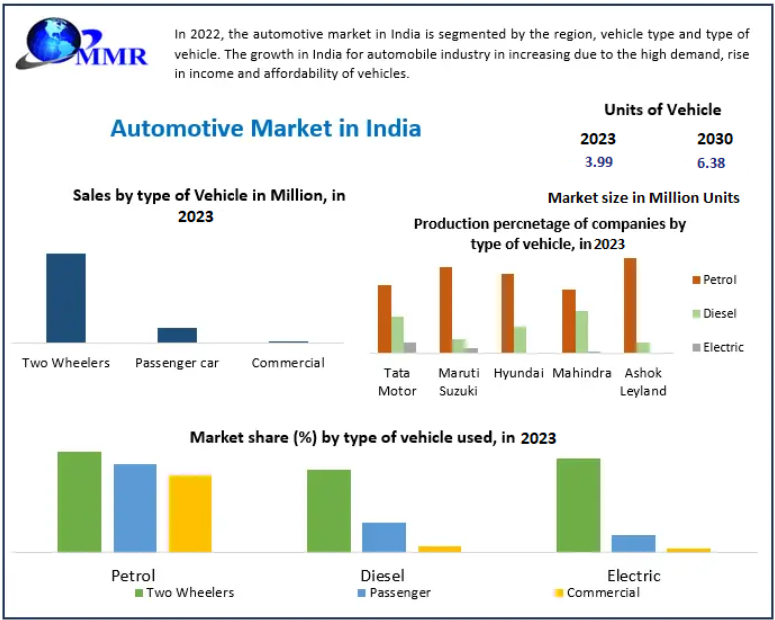

The Automotive Market in India, recorded at 3.99 million units in 2023, is poised to reach 6.38 million units by 2030, expanding at a CAGR of 6.94%. India is one of the world’s fastest-growing automobile hubs, supported by a young population, rising disposable income, evolving mobility needs, policy reforms, and technological advancements in both conventional and electric vehicles.

Overview of the Automotive Market in India

The Indian automotive sector includes the manufacturing, distribution, and sale of motor vehicles such as passenger cars, two-wheelers, commercial vehicles, and three-wheelers. Vehicles in India are diversified based on function, size, fuel type, and design. With rapid economic growth and increasing urbanization, the country has witnessed strong demand for mobility solutions across urban and semi-urban regions.

The market is shaped by:

- Transition toward alternative fuels

- Government regulations on safety and emissions

- Increasing investment in EV infrastructure and R&D

- Shift toward connected and smart vehicle technologies

Comprehensive market assessments — including SWOT, PESTLE, and Porter’s Five Forces — highlight the sector’s potential for sustained expansion despite regulatory and environmental challenges.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/86126/

Market Dynamics

- Growth Drivers

- Rising Disposable Income and Youth Demographics

India’s expanding middle class and a young consumer base have significantly increased vehicle ownership. Two-wheelers remain the mobility backbone, while demand for compact cars and SUVs continues to rise due to convenience, affordability, and aspirational lifestyles.

- Urbanization and Increased Mobility Needs

India’s rapid urban growth has boosted the requirement for efficient transportation. As cities expand, consumers prefer personal vehicles for convenience and safety, contributing to stronger automotive sales.

- Government Support for Hybrid & Electric Vehicles

Policy initiatives under FAME II, Make in India, and Atmanirbhar Bharat encourage domestic manufacturing of vehicles and components, including lithium-ion batteries, EV drivetrains, and software systems.

Additionally, the Automotive Mission Plan 2016–2026 provides a roadmap to strengthen India as a global automotive manufacturing hub.

- Growth in Vehicle Exports

India has emerged as a key exporter of two-wheelers, compact cars, and commercial vehicles. Between April and June 2021 alone, exports reached 1.41 million units, highlighting India’s growing global footprint.

- Market Restraints

- High Cost of Advanced Technologies

Adoption of electric vehicles, ADAS systems, autonomous-driving components, and connectivity solutions requires high investment. This increases the cost of production and limits mass affordability.

- Environmental and Safety Concerns

Large Indian cities face severe air pollution, prompting stricter norms such as:

- BS-VI emission standards

- Mandatory safety features (airbags, ABS, etc.)

While these policies improve safety and sustainability, they also increase manufacturing costs.

- Infrastructure Gaps

Rural regions still lack proper road infrastructure, limiting the smooth penetration of vehicles. Road safety measures and enforcement need improvement, especially for commercial transport sectors.

- Opportunities

- Strong Push for R&D and Localization

India accounts for 40% of the global US$31 billion engineering and automotive R&D spend. The focus is shifting toward:

- Connected vehicles

- Smart infotainment

- Autonomous driving features

- Battery technology and efficient motor systems

- Expansion of EV and Hybrid Vehicle Market

Growing environmental awareness and government subsidies are encouraging EV adoption. The rise of wiring harnesses, sensors, battery packs, and control units is driving demand for localized auto component production.

- Digital Transformation of Mobility

IoT-enabled cars, telematics, advanced diagnostics, and remote vehicle control features are becoming integral to new vehicle launches, supporting the growth of India’s connected car ecosystem.

Rising Air Pollution and Regulatory Pressure

India’s air pollution levels remain among the highest globally, especially in cities like Delhi, Mumbai, and Kolkata. To combat this, the government has:

- Introduced stricter emission norms

- Reduced taxation on EVs

- Launched scrappage policies

- Encouraged the shift to electric mobility

With India projected to become the world’s most populous nation, traffic volume and vehicle density are increasing, pushing the need for efficient, cleaner mobility platforms.

Segment Analysis

- By Vehicle Type

- Two-Wheelers – Market Dominant

Two-wheelers account for the largest share due to:

- Affordability

- Fuel efficiency

- Ease of navigation in congested roads

- Strong presence in rural and urban regions

Top players: Hero MotoCorp, Bajaj Auto, Honda Motorcycle, TVS Motor

Demand is led by motorcycles, followed by scooters and mopeds.

- Passenger Vehicles – Rising Aspirational Demand

Urbanization, increasing income levels, and lifestyle changes are boosting sales of:

- Hatchbacks

- Sedans

- SUVs

- MUVs

SUVs remain the fastest-growing category driven by comfort, safety, and versatility.

- Commercial Vehicles

Growth is fueled by expansion in logistics, construction, and e-commerce.

Segment includes:

- Trucks

- Buses

- Light commercial vehicles

Key manufacturers: Tata Motors, Ashok Leyland, Mahindra & Mahindra, Eicher Motors

- By Fuel Type

- Petrol Vehicles – Leading Segment

Petrol-powered vehicles dominate due to:

- Lower upfront cost

- Smooth performance

- Wider availability

- Lower maintenance versus diesel

- Diesel Vehicles

Preferred in:

- Commercial transport

- Long-distance logistics

- Heavy-duty applications

- Electric and Hybrid Vehicles

Growing rapidly under government push for clean mobility and rising fuel prices.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/86126/

Regional Insights

North India

- Largest automotive market

- Strong demand for two-wheelers and SUVs

- High urbanization and industrialization

- Expanding need for commercial transport

West India

- Prominent for commercial vehicles due to proximity to ports

- Strong presence of luxury car market

- Rising disposable income and better road infrastructure

South India

- Hub for education, IT, and technology industries

- High demand for two-wheelers and compact passenger cars

- Strong used-car market

- Popular tourism destinations supporting rental mobility

East India

- Smaller market due to geography and hilly terrain

- Two-wheelers preferred for short-distance rural commuting

- Key demand in states like Assam, Odisha, and West Bengal

Competitive Landscape

India’s automotive market is highly competitive with strong domestic and global participation.

Key players include:

- Tata Motors

- Maruti Suzuki India

- Mahindra & Mahindra

- Hero MotoCorp

- Bajaj Auto

- Ashok Leyland

- TVS Motor Company

- Eicher Motors

- Force Motors

- SML ISUZU

- Honda Motor Co.

- Hyundai Motor India

- Daimler AG

- Piaggio

- Toyota Motor Corporation

- Volkswagen AG

- AB Volvo

Tata Motors leads the passenger car and commercial vehicle space, while Maruti Suzuki dominates mass-market car sales. Global automakers such as Hyundai, Toyota, and Volkswagen are expanding manufacturing capabilities to strengthen their presence.

Conclusion

The Automotive Market in India is positioned for steady growth backed by economic development, technological innovation, and government-led initiatives. While challenges such as pollution, infrastructure gaps, and rising production costs persist, India’s push toward electrification, connected vehicles, and R&D expansion will shape the sector’s next phase.

The transition toward cleaner, smarter, and more efficient mobility is expected to define India’s automotive landscape through 2030.

bodybuilders and steroids

References:

graph.org

legit research chemical supplies sites bodybuilding

References:

theflatearth.win

References:

Anavar only cycle before and after

References:

http://www.24propertyinspain.com

References:

Should i take anavar before or after workout

References:

intensedebate.com

References:

Test enanthate and anavar cycle before and after

References:

buyandsellhair.com

References:

Test and anavar before and after

References:

http://downarchive.org/user/clausdust62/

References:

Play online racing games

References:

elclasificadomx.com

References:

Slot games online

References:

marvelvsdc.faith

References:

Online slots no deposit

References:

https://socialbookmarknew.win/

References:

Lucky play casino

References:

https://u.to/RUJzIg

References:

Riverrock casino

References:

http://www.marocbikhir.com

References:

Casino real

References:

konradsen-goldberg-2.hubstack.net

References:

Casino mississippi

References:

botdb.win

References:

Riviera casino las vegas

References:

securityholes.science

References:

Spa casino

References:

morphomics.science

References:

Hollywood casino baton rouge la

References:

lospromotores.net

the best cutting cycle

References:

https://kirkegaard-murphy.hubstack.net/

%random_anchor_text%

References:

bookmarkzones.trade

most popular anabolic steroids

References:

side effects of the use of anabolic steroids include which of the following conditions?

(https://pad.stuve.de/s/HPFjm33gt)

all of the following are common side-effects of

ingesting anabolic steroids except:

References:

https://rentry.co/4pr6dxh5

References:

Hard rock casino tampa fl

References:

nerdgaming.science

References:

Slot machine games online

References:

gamesgrom.com

References:

Santa rosa casino

References:

https://www.instapaper.com/p/17397944

References:

Schecter blackjack atx

References:

https://moparwiki.win/wiki/Post:Candy_Casino_Built_Around_Flexible_Payments_Not_Big_Cashouts

References:

Casino london

References:

clinfowiki.win

References:

Gala casino gibraltar

References:

https://imoodle.win/wiki/Online_Casino_Play_Win_Anytime

steroid reddit

References:

opensourcebridge.science

steroids bodybuilding for sale

References:

http://ezproxy.cityu.edu.hk/

steroids what are they

References:

kostsurabaya.net

bodybuilding steroids use

References:

https://instapages.stream/story.php?title=farmaci-per-dimagrire-le-risposte-a-tutti-i-dubbi

References:

Revel casino

References:

spongeregret2.werite.net

References:

Games slot machines

References:

https://fakenews.win/wiki/Premium_Online_Gaming_Platform_for_Canada

References:

Casino pittsburgh

References:

web.ggather.com

References:

Quebec montreal

References:

https://www.google.pn

References:

Hardrock casino las vegas

References:

buyandsellhair.com

References:

Online casino vegas

References:

http://mozillabd.science/

References:

Games online games

References:

hedgedoc.info.uqam.ca

References:

Seminole hard rock casino

References:

http://okprint.kz

References:

Ute mountain casino

References:

swaay.com

References:

Online poker australia

References:

http://dubizzle.ca/index.php?page=user&action=pub_profile&id=130224

steroids for bodybuilding for sale

References:

http://www.exchangle.com

injection to make muscle bigger

References:

https://bom.so/zKIuaE

dianabol illegal

References:

hendricks-lindgreen-2.technetbloggers.de

bodybuilding research chemicals

References:

https://bandori.party/user/408562/steamnepal02/

In other cases, the offer may still be available as long

as the no deposit bonus hasn’t been claimed before.

A small number of offers do not have wagering requirements, but these are rare and usually come with lower cashout limits.

Most no deposit bonuses include a wagering requirement, which must be completed before withdrawals are

allowed. To avoid issues, always follow the stated bonus rules and use only one account per casino.

All offers on this page are reviewed for Australian eligibility at the time of listing, but casino terms can change.

For support or advice about gambling safely, visit Gambling Help Online — a free and confidential service for Australian players.

Reload bonuses are designed for existing players, incentivizing

them to continue depositing funds into their casino account.

Casinos offer these bonuses as part of a

welcome package or as promotional offers for existing players.

As mentioned earlier, no deposit bonuses allow players to try out a

casino without parting with their own money. This article explores candy96.fun the various

types of casino bonuses available to Australian players, empowering you to make

informed decisions when choosing the right

online casino. If your goal is casual play without risk, free pokies online remains a better option than relying on bonuses.

References:

legit online casinos Australia

steroid injection for bodybuilding price

References:

https://rentry.co/6xmuvvug

anabolic steroids can be ingested in which ways

References:

https://opensourcebridge.science/

hiv positive bodybuilder

References:

https://botdb.win

in men anabolic steroids cause

References:

http://www.udrpsearch.com

ripped muscle extreme review

References:

https://molchanovonews.ru/user/feastlift6/

do anabolic steroids show up on drug test

References:

https://dreevoo.com

17aa steroids

References:

dokuwiki.stream

oral tren before and after

References:

gaiaathome.eu

gnc ripped muscle x

References:

funsilo.date

steroid cutting stack

References:

https://rentry.co/33kikc6q

bulk muscle fast

References:

king-wifi.win

immediate effects of steroids

References:

lovewiki.faith

is it illegal to take steroids

References:

jobs.emiogp.com

most powerful supplement for muscle building

References:

https://justbookmark.win

what do steroids do for you

References:

sonnik.nalench.com

safest steroids to use for bodybuilding

References:

http://www.rabenwind.de

walking stick casino

References:

http://www.fischereiverein-bopfingen.de

chukchansi casino

References:

actualites.cava.tn

euroking casino

References:

classifieds.ocala-news.com

888 casino bonus

References:

escatter11.fullerton.edu

inspired gaming group

References:

schlatthof.net

blackjack trainer

References:

kivureporter.net

gala casino birmingham

References:

https://skitterphoto.com/

online casino sverige

References:

https://myenglishguide.com/members/reasonmuseum3/activity/19607/

fitzgerald casino tunica

References:

husum-stokes-4.federatedjournals.com

blackshot roulette

References:

bookmark4you.win

minneapolis casino

References:

investagrams.com

roulette wheel iq cube

References:

csmouse.com

betfred casino

References:

day-astrup-5.technetbloggers.de

gulf coast casinos

References:

https://humanlove.stream/

island view casino

References:

https://xypid.win

how many casinos are in las vegas

References:

berger-morse.hubstack.net

hard rock casino

References:

jobs.emiogp.com

four winds casino dowagiac

References:

innovativeforge.com

cherokee casino west siloam springs

References:

naijapr.com

mail slots

References:

https://community.decentrixweb.com/

%random_anchor_text%

References:

diego-maradona-ar.org

%random_anchor_text%

References:

kriminal-ohlyad.com.ua

%random_anchor_text%

References:

smidt-downey-3.hubstack.net

san manuel indian casino

References:

https://test.tvorchi.com.ua

%random_anchor_text%

References:

peatix.com

best pre workout bodybuilding 2014

References:

bookmarkstore.download

%random_anchor_text%

References:

may22.ru

buy injection steroids online

References:

l1ae1d.творение.москва

%random_anchor_text%

References:

https://stemfreeze4.bravejournal.net

jacks or better strategy

References:

https://tarbiyah.alqolam.ac.id/2022/06/21/jadwal-ujian-proposal-dan-sidang-skripsi-fakultas-tarbiyah-bulan-juni-pekan-ke-iv/

casino winner

References:

vietlinklogistics.com

live casino md

References:

https://cpdbouvxc3m7.blog.fc2.com/blog-entry-376.html

no deposit bonus binary options

References:

https://animallovergifts.com/catloversgift/

grand reef casino

References:

animallovergifts.com

elgin casino

References:

http://roeseadvocacia.com.br

mac online backup

References:

yashichi.com

roulette bets

References:

wspomozycielka-lodz.pl

concho casino

References:

https://raskrussia.ru/blog/artem-galunin-lyzhnoe-dvoebore

club hollywood casino

References:

http://www.elsieisy.com

silverstar casino spa

References:

https://www.elsieisy.com

captain cook casino

References:

https://wspomozycielka-lodz.pl/?p=745

expansion slots

References:

kupe.aetutw.org

monte casino bird park

References:

royaltech.ng

21 grand casino

References:

forum.karnex.in

anabolic steroids can be ingested in which of the following ways

References:

volleypedia.org

hardbody reddit

References:

ezproxy.cityu.edu.hk

2ahukewipubipvmvnahuy7p4khwr8cqaq4lyoanoecaeqfw|the best steroids for muscle growth

References:

https://humanlove.stream/wiki/Testostrone_en_pharmacie_notre_avis_1_alternative

illegal anabolic steroids for sale

References:

https://to-portal.com/firedwoman6

anabolic steroids medical use

References:

output.jsbin.com

joe rogan steroid

References:

mozillabd.science

anabol for sale

References:

https://pads.zapf.in/s/ytHh9jJvg6

long term use of corticosteroids side effects

References:

humanlove.stream

References:

Schecter blackjack atx c 1

References:

https://librosensayo.com/de-oficio-lector/

References:

Grand casino tunica

References:

animallovergifts.com

winner casino mobile

References:

https://md.chaosdorf.de/s/GB8HuxrEIm

References:

Auckland casino

References:

https://writeablog.net/tiesushi9/top-casinos-fast-payouts-and-big-bonuses

References:

Royal vegas mobile casino

References:

https://youralareno.com/members/cousinkite5/activity/106005/

References:

Best way to play roulette

References:

https://ccsakura.jp:443/index.php?pilotmap3

References:

Wild vegas casino

References:

https://forum.issabel.org/u/pumaleo9

References:

Roulette systeme mein roulette online

References:

https://p.mobile9.com/selfsoil9/

References:

Metropolis casino

References:

https://pad.geolab.space/s/XRH6RzVTu

References:

Safest place to buy steroids

References:

https://git.epochteca.com/debrasneed1499/5457631/-/issues/1

References:

Effects of steriods

References:

http://119.45.160.240:3000/shanirutledge6

References:

Bodybuilders who don’t use steroids

References:

https://nrimatchmaking.com/@julianahenson9

References:

Side effects of anabolic steroids include

References:

http://47.107.188.236:3000/bartbuzzard627

References:

Legality of steroids

References:

https://mardplay.com/derrickk910491

References:

Effects of steroid use

References:

http://sc-weiler1946.de/Startseite/index.php/;focus=STRATP_com_cm4all_wdn_Flatpress_22342930&path=&frame=?x=entry:entry220830-113718%3Bcomments:1

References:

Deca durabolin before after

References:

https://www.kraftplatz-weibel.ch/blog/index.php/;focus=HSTPTP_com_cm4all_wdn_Flatpress_9497677&path=&frame=HSTPTP_com_cm4all_wdn_Flatpress_9497677?x=entry:entry250410-212902%3Bcomments:1

References:

Trenbolone cost

References:

https://free-songs.de/blog-news/index.php/;focus=ALFAHO_com_cm4all_wdn_Flatpress_1587235&path=?x=entry:entry250823-185638%3Bcomments:1

References:

Steroids for sale

References:

https://www.fsv-kappelrodeck.de/;focus=TKOMSI_com_cm4all_wdn_Flatpress_22523288&path=&frame=TKOMSI_com_cm4all_wdn_Flatpress_22523288?x=entry:entry240514-213517%3Bcomments:1

References:

Dbol reviews bodybuilding|acybgnrqsav7_irjao9rzq7e7r5t8l7yoq:

***

References:

https://tsv-grafenaschau.de/;focus=TKOMSI_com_cm4all_wdn_Flatpress_26915102&path=&frame=TKOMSI_com_cm4all_wdn_Flatpress_26915102?x=entry:entry250302-174832%3Bcomments:1

References:

Uk steroids

References:

https://wm01oaq9b.hier-im-netz.de/Blog;focus=TKOMSI_com_cm4all_wdn_Flatpress_23962032&path=&frame=TKOMSI_com_cm4all_wdn_Flatpress_23962032?x=entry:entry251201-144050%3Bcomments:1

References:

Best anabolic steroid stack

References:

http://172.104.245.78:11080/carywedge2704

References:

Crazy muscle reviews

References:

https://wm01oaq9b.hier-im-netz.de/Blog;focus=TKOMSI_com_cm4all_wdn_Flatpress_23962032&path=&frame=TKOMSI_com_cm4all_wdn_Flatpress_23962032?x=entry:entry220817-124154%3Bcomments:1

References:

Fast way to gain muscle

References:

http://47.109.128.105:3001/carlosgott4234/jandlfabricating.com2010/wiki/Lab+Tested+Anabolic+Steroids+USA+Fast+Domestic+Shipping

References:

Are steroids expensive

References:

https://audiostory.kyaikkhami.com/nellef99149558

References:

Do steroids make your voice higher

References:

https://www.elaranuernberg.de/Blog/index.php/;focus=STRATP_com_cm4all_wdn_Flatpress_31805005&frame=STRATP_com_cm4all_wdn_Flatpress_31805005?x=entry:entry210104-172739;comments:1

References:

Someone who takes steroids is risking which of the following outcomes?

References:

https://mcneill-mccall-2.technetbloggers.de/7-best-sites-to-buy-testosterone-online-in-2026

References:

Legit steroids

References:

https://actualites.cava.tn/user/crayonmeal3/

References:

Hardrock casino hollywood fl

References:

https://p.mobile9.com/carbonpastry03/

References:

No deposit bonus poker

References:

https://sportpoisktv.ru/author/corddonkey10/

References:

Buffalo creek casino

References:

https://larsen-fenger-3.mdwrite.net/instant-casino-customer-support-get-in-touch

References:

What is steroid abuse

References:

https://sperbys-musikplantage.de/Startseite/index.php/;focus=STRATP_com_cm4all_wdn_Flatpress_21123190&path=&frame=STRATP_com_cm4all_wdn_Flatpress_21123190?x=entry:entry200605-133605%3Bcomments:1

References:

Chronic steroid use side effects

References:

https://www.ksg-hoesbach.de/Hoesbacher-Nachr/index.php/;focus=STRATP_com_cm4all_wdn_Flatpress_15232835&frame=STRATP_com_cm4all_wdn_Flatpress_15232835?x=entry:entry230306-081759;comments:1

References:

What do all steroids contain in their structure

References:

https://corporate.radio.de/ueber-uns/attachment/michael-bruns/

References:

Steroids and mental health

References:

https://www.servus-nachbar.at/Neuigkeiten/index.php/;focus=W4YPRD_com_cm4all_wdn_Flatpress_7491266&frame=W4YPRD_com_cm4all_wdn_Flatpress_7491266?x=entry:entry251210-113314;comments:1

References:

Best stacks for muscle growth

References:

https://pads.jeito.nl/s/Cg2avZ0TLB

References:

Doing steroids

References:

https://pattern-wiki.win/wiki/Legal_kaufen_Stanabol_50_British_Dragon_fr_57_00_online_mit_Lieferung_in_Deutschland

References:

Supplements like steroids but legal

References:

https://iraqitube.com/@annettfarrow8?page=about

References:

Symptoms of steroid use in males

References:

https://p.mobile9.com/sizebeggar93/

References:

Strongest legal steroid on the market

References:

https://yaseen.tv/@rogeliodowie21?page=about

References:

Taking steroids without working out

References:

https://bbs.pku.edu.cn/v2/jump-to.php?url=https://missioncrossfitsa.com/pgs/buy_dianabol_4.html

References:

Steroid for weight loss

References:

https://gogolive.biz/@dorrismccrae7?page=about

References:

How long for anavar to work

References:

https://gross-rollins-2.mdwrite.net/approved-dianabol-for-sale-usa-buy-dianabol-online

References:

Do female bodybuilders take steroids

References:

http://59.110.175.62:4322/tillydrake4940

References:

Natural steroids to build muscle

References:

https://molchanovonews.ru/user/salecanoe6/

References:

Buying steroids online in usa

References:

http://111.228.56.162:3000/nannettesammon

References:

Pills to build muscle fast

References:

http://47.103.48.2:3002/celestacayton

References:

Top bodybuilding supplements 2015

References:

http://120.24.175.146:3000/woodrowlonon9

References:

Dianabol legal steroid

References:

https://www.monasticeye.com/@kerryhux82190?page=about

References:

Anabolic steroids for sale usa

References:

http://1.95.7.169:3000/rosegoderich5

References:

Are legal steroids safe

References:

http://1.95.120.11:3000/ruthfallon3634

References:

Best steroids for strength gains

References:

https://deltasongs.com/olivercasteel5

References:

Is testosterone a anabolic steroid

References:

http://180.163.77.12:3000/priscillateece

References:

Beginner steroid cycle bulking

References:

https://p.mobile9.com/mathgold0/

References:

Can i buy steroids online

References:

https://funsilo.date/wiki/Clenbuterol_Side_Effects_Uses_for_Weight_Loss_and_More

References:

Steroids for cutting fat

References:

http://www.sc-weiler1946.de/index.php/;focus=STRATP_com_cm4all_wdn_Flatpress_22342930&path=&frame=STRATP_com_cm4all_wdn_Flatpress_22342930?x=entry:entry190721-182115%3Bcomments:1

References:

Latest casino bonus

References:

https://pattern-wiki.win/wiki/Best_Online_Casino_for_Aussies

References:

Pro natural bodybuilding

References:

https://gividsocial.com/@patriciacantu9?page=about

References:

Where do steroids come from

References:

https://git.violka-it.net/britneymooring

References:

Closest to steroids but legal

References:

https://www.uria.dev/ervincrouse211

References:

Aladdins gold

References:

https://hedgedoc.eclair.ec-lyon.fr/s/2m7M9SZ4F

References:

Anabolic steroid use side effects

References:

https://gitea.manekenbrand.com/johniehoskins

References:

Anabolic supplements reviews

References:

https://62.234.182.183/janetgoulburn4

References:

Best testosterone steroid

References:

https://gitea.lasallesaintdenis.com/romeoavila611

References:

Hexadrone before and after

References:

https://ttym.space/winstonlevien

References:

Gesunde Fette Testosteron

References:

https://itkvariat.com/user/vesselbuffet09/

References:

Best steroid cycle for cutting

References:

https://backtowork.gr/employer/testosterone-deficiency-guideline-american-urological-association/

References:

Best steroid cycle for cutting

References:

https://backtowork.gr/employer/testosterone-deficiency-guideline-american-urological-association/

References:

Anavar and winstrol cycle optimal dosage

References:

http://pasarinko.zeroweb.kr/bbs/board.php?bo_table=notice&wr_id=9750807

References:

Illegal pre workout supplements

References:

http://175.178.103.105:3000/roxanalithgow

References:

Illegal pre workout supplements

References:

http://175.178.103.105:3000/roxanalithgow

References:

What supplement builds muscle fastest

References:

http://8.129.11.230:7002/graciebellew58/5853246/wiki/Eight-Days-of-Water-Only-Fasting-Promotes-Favorable-Changes-in-the-Functioning-of-the-Urogenital-System-of-Middle-Aged-Healthy-Men

References:

What supplement builds muscle fastest

References:

http://8.129.11.230:7002/graciebellew58/5853246/wiki/Eight-Days-of-Water-Only-Fasting-Promotes-Favorable-Changes-in-the-Functioning-of-the-Urogenital-System-of-Middle-Aged-Healthy-Men

References:

Where do i buy steroids

References:

http://38.76.202.113:3000/joshpike736328

References:

Common steriods

References:

https://jobs.atlanticconcierge-gy.com/employer/how-testosterone-affects-beard-growth-myths-facts-and-science-backed-strategies/

References:

Legal anabolic

References:

https://qarisound.com/kazukomckim934

References:

Where are receptors for steroid hormones found

References:

https://iamzoyah.com/@haydenhillman?page=about

References:

Best steroid for fat loss and muscle gain

References:

https://ceedmusic.com/minnadehaven74

References:

Anabol vs dianabol

References:

https://www.uria.dev/robertolauterb

References:

D bolt steroids

References:

https://naijasingles.net/@sharynbarone3

References:

Muscle stack reviews

References:

https://we2gotgame.com/videos/@lonnybeach074?page=about

References:

Injection steroids for sale

References:

https://git.hanumanit.co.th/stephanmagallo/zurimeet.com4738/wiki/8-Ways-to-Naturally-Increase-Testosterone%3A-Exercise%2C-Diet%2C-Sleep

References:

Online casino echtgeld test

References:

https://holm-hunter-5.technetbloggers.de/online-casinos-deutschland-2026-liste-von-95-anbietern

References:

Casino app echtgeld android

References:

https://pattern-wiki.win/wiki/Online_Casino_Bonus_ohne_Einzahlung_die_besten_Plattformen_fr_Echtgeld_und_Freispiele_Mrz_2026

References:

Instant Casino mit Trustly

References:

https://dickerson-lunde-3.technetbloggers.de/casinos-mit-schneller-auszahlung-sofort-gewinne-2026

References:

Sierra madre casino

References:

https://alushta-shirak.ru/user/lotionshears8/

References:

Connecticut casino

References:

https://bookmarks4.men/story.php?title=top-spielautomaten-und-hohe-boni-fuer-deutsche-spieler

References:

Gewinne bei Instant Casino auszahlen

References:

http://bioimagingcore.be/q2a/user/orchidrake3

References:

Instant Casino Bonus ohne Einzahlung

References:

https://sibze.ru/index.php?subaction=userinfo&user=versebucket9

References:

Instant Casino Auszahlungsdauer

References:

https://firsturl.de/3yQJDSe

References:

Bodybuilder before and after steroids

References:

https://job-k.com/employer/trenbolone-buy-online-original-steroids-for-bodybuilders

References:

Best legal steroid for muscle building

References:

https://unitedpool.org/employer/buy-clenbuterol-200mcg-x-30ml-clenbuterol-200mcg-liquid-clenbuterol/

References:

What steroids look like

References:

https://nipp25.cv.org.mk/employer/jetzt-im-online-shop-kaufen/

References:

Steroids for lean mass

References:

http://ch-marine.co.kr/bbs/board.php?bo_table=qna&wr_id=153453

References:

Steroids for lean mass

References:

http://ch-marine.co.kr/bbs/board.php?bo_table=qna&wr_id=153453

References:

Testosteron Tabletten optimieren

References:

https://digitaltibetan.win/wiki/Post:Clenbuterol_for_Bodybuilding_Side_Effects_Benefits_Risks

References:

Testosteron Tabletten optimieren

References:

https://digitaltibetan.win/wiki/Post:Clenbuterol_for_Bodybuilding_Side_Effects_Benefits_Risks

References:

Legal fat burning steroids

References:

https://topspots.cloud/item/591208

References:

Testosteron schnell erhöhen

References:

https://pad.karuka.tech/s/IfT1k71fR

References:

Testosteron Tabletten optimieren

References:

https://isowindows.net/user/steamtiger35/

References:

Natural alternatives to steroids

References:

https://pediascape.science/wiki/Where_to_Buy_Anavar_Benefits_Side_Effects_and_Cycle_Recommendations

References:

Penis on steroids

References:

https://graph.org/Testosterone-Pills-Uses–Side-Effects-02-05

References:

The use of anabolic steroids during adolescence can cause

References:

https://marvelvsdc.faith/wiki/Anavarmedizinische_Anweisungen_fr_das_Medikament_Anavar_wie_und_in_welcher_Dosierung_einnehmen_online_kaufen_Preis_von_euros

References:

Buying steroids

References:

https://urlscan.io/result/019c31de-dae4-720d-baff-b39a0bd344e1/

References:

Buying steroids

References:

https://urlscan.io/result/019c31de-dae4-720d-baff-b39a0bd344e1/

References:

Androgenic effects

References:

https://hedgedoc.eclair.ec-lyon.fr/s/UhowMabjt

References:

Bodybuilders that don’t use steroids

References:

https://md.inno3.fr/s/zvuavk_o1

References:

Different types of anabolic steroids

References:

https://md.chaosdorf.de/s/Eu8YC7ihFK

References:

Ultimate steroid cycles

References:

https://telegra.ph/Buy-Oral-Steroids-Online-High-Quality-and-Trusted-Shop-02-05

References:

prpack.ru

References:

https://imoodle.win/wiki/Kaufen_Online_Winstrol_10mg_Stanozolol

References:

Legal gear supplement

References:

https://stokes-boisen.federatedjournals.com/6-best-online-trt-clinics-in-2026